“Everyone talks about building a relationship with your customer. I think you build one with your employees first.”

According to Angela Ahrendts, the former VP of Apple, this is what the main focus of companies should be.

There is no doubt that motivated and capable associates and employees are the essence of every business. During the dot-com revolution in the late 90s among startups and companies in the USA (especially in the IT industry) it became common for employers to offer their employees the possibility to get the companies’ share. In this way, employees, management, and consultants got a chance to become partners with the company’s founders and owners.

Specifically, over 6,500 companies in the USA have an Employee Stock Ownership Plan (hereinafter: ESOP ), and almost 15 million American employees are part of the ESOP system.[1]

What is this really about? ESOP (similar to “stock options” in the US practice) is used as a term for an arrangement in which an employee of a company may acquire the shares of the company, under certain conditions. This broad concept, which is also known in practice as vesting, can take various forms, ranging from simple grants of shares to highly structured plans.

With the accelerating development of the IT industry, and especially with the strengthening of startups, a need for ESOP has emerged in Serbia as well. Still, the appropriate legal framework initially was not created. Same as before, the legal system once again hindered the functioning of companies and contemporary development.

However, in April 2020, the amendments to the Companies Act (hereinafter: CA) came into force, and Serbia became one of the countries where companies offer their employees and other partners the option to become shareholders under preferential conditions after a certain period of time.

In other words, on a precise day in the future, your employees will be able to become shareholders in your company at an in-advance determined price, and in return, employees will be motivated to work harder and thus, increase the value of your company.

During an economic crisis, when opportunities for traditional benefits like bonuses become limited, this option could be a game-changer for your company.

Models of ESOP in Serbia

In practice, there are two main models through which employees can be granted a share in a company:

- Acquiring a Share in a Domestic Company

This model involves a domestic company (for example a Serbian company) allowing its employees to acquire shares in the same company. This model is often simpler from a regulatory perspective since the transactions occur within the same jurisdiction. However, from a tax perspective, this model can be more expensive for the company, which is why domestic companies often turn to the second model explained below.

- Acquiring a Share in an Affiliated Foreign Company

The second option is for domestic employees to acquire shares in the parent or affiliated company located abroad. For example, employees of a Serbian company may be granted the right to acquire shares in the U.S. parent company that owns the Serbian company. This model is commonly used in international companies and can provide additional benefits to employees, especially if the foreign company is already well-established in the market and has greater growth opportunities. However, the regulatory and tax implications of such a model should be carefully considered.

The choice of model depends on the company’s structure, the objectives of the employee incentive program, and the legal and tax aspects, all of which need to be carefully analyzed before making a decision.

In this text, we will analyze in more detail the first model, i.e., acquiring a share in a domestic company.

How to Provide Employees with the Possibility to Acquire Shares?

If you consider that this kind of employee incentive would work for your company, you must enforce the entire procedure by the law.

Specifically, the CA defines in detail the procedure for providing employees with the possibility to participate in ESOP and we will explain the key terminology and some of the most important steps for implementation of this plan.

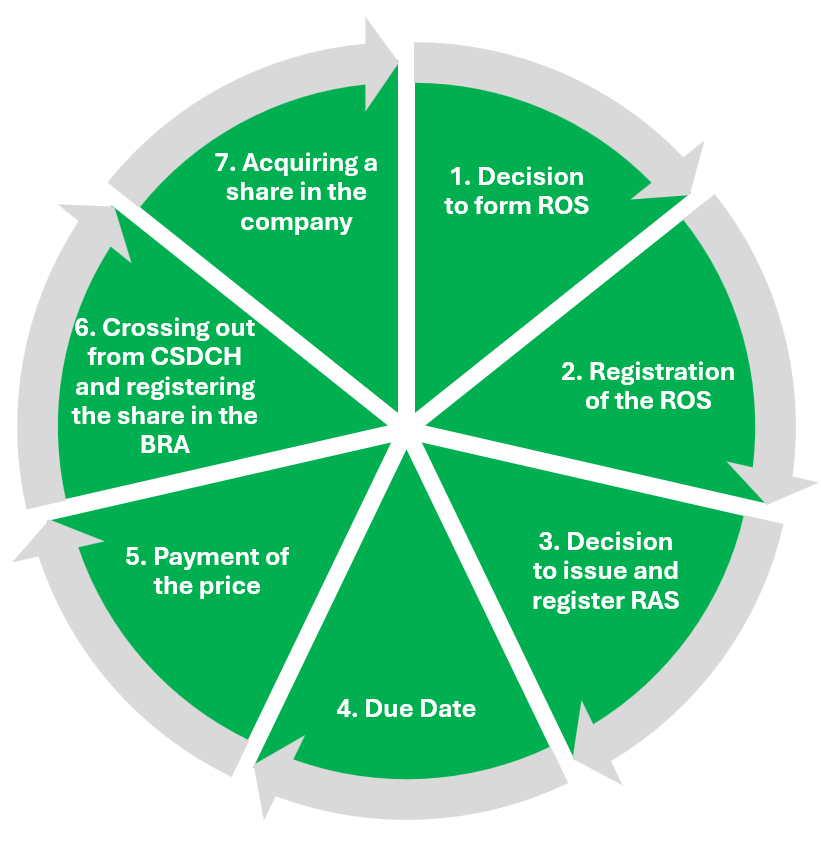

To start the procedure, it is necessary to enact the Decision on Establishing the Reserved Own Share. The Reserved Own Share (hereinafter: ROS) is the share that the company gains from its members without compensation, which should be registered with the Business Registers Agency (hereinafter: BRA).

It is important to note that the company can acquire ROS only from shares of members whose deposits were entered/paid fully and can be formed only with the shares of those members who have voted for rendering the Decision on Establishing the Reserved Own Share. The consequence of the General Assembly’s decision on the acquisition of ROS is that the shares of members who have voted for will decrease.

Afterward, the company can take the next step and issue the financial instruments – so-called rights to acquire shares (hereinafter: RAS). RAS is issued based on the Decision on Issuance of the Financial Instrument – the Right to Acquire Shares, which should be registered with the Central Securities Depositary and Clearing House (hereinafter: CSDCH).

The right to acquire shares i.e. RAS is a non-transferable financial instrument that, for example, allows an employee to acquire a certain percentage of a company’s shares on a certain day at a certain price, without the possibility of the other members of the company using their pre-emptive rights to purchase shares. The price at which, based on the PSU, employees will be able to acquire shares, can be symbolic and amount to RSD 1.

Once the RAS matures, the holder of the financial instrument must pay the agreed price, in order to acquire the company’s shares. Afterward, the financial instrument is removed from CSDCH, and the holder of the financial instrument – for example, your employee, is registered as a shareholder of the Company in the BRA. Simultaneously, the ROS balance is reduced by the same percentage as the share acquired through the RAS.

What should you pay attention to?

Besides the complex procedure, CA prescribes a number of specifications for this action and the treatment of ROS, i.e. RAS.

Unlike regular company shares, which can be freely pledged or transferred under the general legal framework, RSUs cannot be used as collateral or transferred to another party. Also, in order to establish ROS, the company does not have to increase the share capital, because the ROS will be established from the already entered/paid capital.

Another particularity is the possibility that a single-member company can acquire ROS. Therefore, even if your company has only one member, you can still opt for this model, ultimately transforming it into a multi-member company.

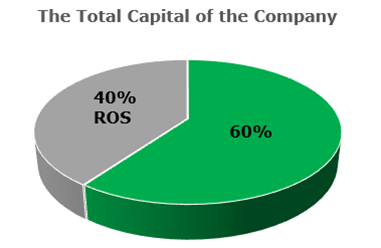

Additionally, it is also important to note that it is possible to issue multiple ROSs that do not merge into one share, but rather different ROSs exist, with a restriction of the maximum percentage of shares of all ROSs in the share capital of the company which cannot exceed 40%.

One of the benefits provided by the CA is that there is no mandatory deadline for issuing RAS from a registered ROS. ROSs must issue RASs, by which a possibility was given to the company. This flexibility allows companies to tailor the issuance process to their specific needs. It’s entirely possible that a company may abandon the idea of issuing financial instruments after establishing a ROS for that purpose. In such cases, a ROS from which no financial instruments have been issued can either be split into multiple new ROSs or canceled altogether.

When it comes to who can hold an RAS, the CA does not impose any restriction that it must be your employee. Instead, it can be any individual outside your company—external collaborators, business partners, friends, or even completely unrelated third parties. Additionally, the RAS holder can be either a domestic or foreign individual or legal entity. However, it is essential to formalize the relationship with the holder of RAS by an appropriate written agreement by which the conditions of share acquisition will be regulated.

It is important to emphasize that a RAS is tied to a specific individual—the rights holder. In other words, a RAS cannot be pledged as collateral or inherited. For example, if you designate your employee John Doe as the RAS holder, they will not be able to use the RAS as security or transfer it through inheritance.

ESOP Pros (and Cons)

The key advantage of this system is that it is designed to boost employee engagement and motivation, driving them to achieve the best possible results for the company.

One of the strongest incentives for employees is the opportunity to become shareholders, allowing them to sell their shares or participate in company profits, potentially leading to additional financial benefits.

Moreover, when an employee holds shares in the company, they are more likely to be invested in its success, as a thriving business directly increases both the company’s overall value and the worth of their shares.

Additionally, employee share ownership fosters long-term commitment, reducing the likelihood of turnover. This is particularly valuable in the IT sector, where retaining top talent is a major challenge. By implementing this mechanism, companies can strengthen employee loyalty and secure the stability of their best teams.

On the other hand, from a strictly commercial point of view, someone could argue that the main “lack” of this model is the price at which the employees will have the right to purchase a share. This price could be drastically lower than the market price at the time of the acquisition, which reduces the amount of compensation from the future value of the company.

In other words, at that moment when you issue RAS, you can arrange with the employees that on May 2025, they will have the right to acquire a part of the shares of the company for EUR 50. A realistic scenario is that that exact share is worth EUR 500 on May 2025, however, the employee will have a right to purchase that share at a preferential price.

Nevertheless, this can rather be seen as an investment in employees and, if Apple’s former VP is to be believed, probably the best one a company can do.

A Win-Win Situation

It is crucial to carefully evaluate whether reserving shares is the right move for your company by conducting a comprehensive financial and strategic analysis of your business. Additionally, special attention must be given to the tax implications of this mechanism, as different models come with varying tax treatments.

That being said, while the process may seem complex due to unfamiliar terminology and intricate procedures, with the right professional guidance, you can navigate it smoothly and achieve a win-win outcome.

For employers, this approach fosters a more engaged and motivated workforce, while employees gain the opportunity to benefit financially by making a relatively small investment.