Personal Income Tax Serbia Changes in 2026 – What It Means for Your Business

Accelerated updates in tax legislation present significant challenges but also open new opportunities for business owners. The amendments to the Personal Income Tax Law (hereinafter: “Law“), which are effective from January 2025, introduce substantial changes across various aspects. It is crucial to examine how these new rules impact businesses and their financial planning. This article sheds light on only a part of the amendments relevant from the perspective of the Law, while other key tax regulations, such as the Corporate Income Tax Law and the Law on Tax Procedure and Tax Administration, have also undergone significant revisions.

Are you ready to adjust your strategies to these changes? This blog provides a comprehensive overview of the key amendments to the Law that will mark 2025, offering you practical advice for compliance and tools that will help you take timely action.

Proactivity is key, because when it comes to taxes, even the smallest detail can make a difference between cost optimization and unwanted consequences.

Amendments to the Personal Income Tax Law for 2025

With the onset of 2025, the Republic of Serbia is introducing significant changes to the Law, which will have a direct impact on employers, employees, and specific professions such as seafarers. These changes require careful planning and adjustment to ensure compliance with the new regulations and to fully utilize the benefits and incentives that the Law provides.

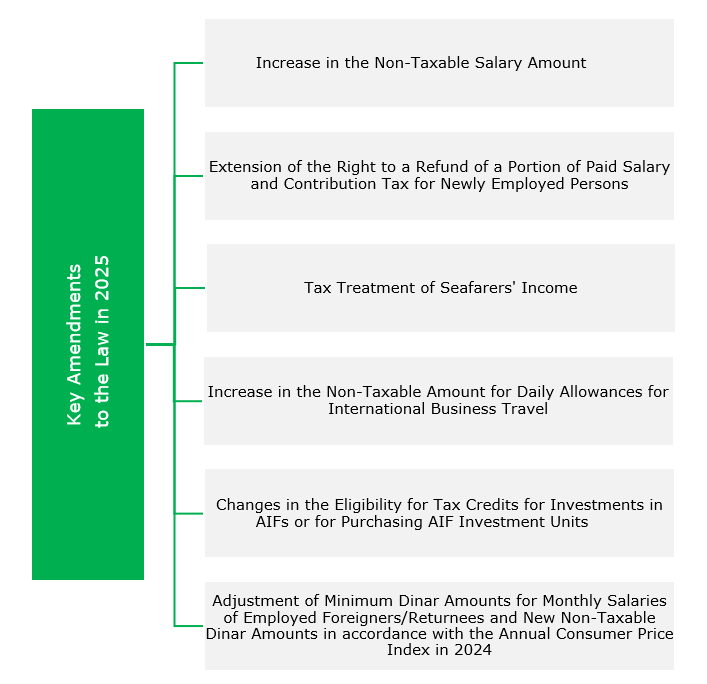

Specifically, the changes include:

a) Increase in the non-taxable amount of salaries;

b) Extension of the right to a refund of a portion of the paid tax and contributions on salaries for newly employed persons;

c) Detailed tax regulation on the treatment of seafarers’ income;

d) Increase in the non-taxable amount for daily allowances for business trips abroad;

e) Introducing new conditions for the tax incentives for investments in AIFs;

f) Increase in the minimum dinar amounts of monthly salaries for foreign employees and returnees, which are necessary to qualify for tax incentives; and

g) New aligned dinar non-taxable amounts of personal income tax with the annual consumer price index in 2024.

1) Increase in the Non-Taxable Amount of Salaries

One of the most significant amendments to the Law is the increase in the non-taxable monthly amount of salaries from the previous RSD 25,000 (~ 210 EUR) to RSD 28,423 (~ 240 EUR). This change leads to a reduction in the tax base applied to salaries, which directly results in a lower tax obligation for the employer.

UPDATE IN 2026: From the moment this text was first published, the non-taxable amount of salary has been adjusted, so in 2026 it amounts to 34.221 RSD (~ 290 EUR).

It is important to note that this increase does not require an automatic amendment to the employment agreement. Employment agreements always stipulate the gross amount of the salary, but may also include the net amount, while tax policy is applied independently of these provisions. Therefore, employers are not obligated to change existing employment agreements with employees due to this tax innovation.

In practice, this means that the tax base for salary taxes will decrease, leading to a lower amount of tax when the tax rate is applied to the reduced base. As a result, employers will have a lower tax obligation, while the contracted gross amounts of salaries remain unchanged.

EXAMPLE: Consider an employee with a gross salary of RSD 100,000. Before the amendment, the non-taxable amount was RSD 25,000, meaning that tax was calculated on a base of RSD 75,000. With a tax rate of 10%, this meant that the employer paid RSD 7,500 in salary taxes. However, with the new non-taxable amount, the tax base is now lower – RSD 65.779. Applying the same tax rate of 10% results in a tax of RSD 6.578, meaning that the employer’s tax obligation is now lower. This difference may seem small on an individual level, but when applied to the total salaries of employees in a company, the effect becomes significant.

However, employers are required to adjust salary calculations in accordance with the new non-taxable amount. This involves updating internal payroll systems to properly apply the new non-taxable amount.

It is noted that the alignment of the non-taxable amount of salaries with the annual consumer price index occurs every year.

2) Extension of the Right to Refund a Portion of Paid Tax and Contributions on Salaries for Newly Employed Persons

Certain tax incentives available for employers who meet specific conditions have been extended until 31 December 2025:

- A tax incentive that allows an employer to refund a portion of the paid tax and contributions on salaries if it employs a person who qualifies as newly employed (at rates of 65-75% of the paid tax and contributions, depending on the number of newly employed persons employer enters into employment relationship); and

- A tax incentive that enables an employer who establishes an employment relationship with at least two new persons qualifying as newly employed to a refund of 75% of the paid tax and contributions on salary for such newly employed person.

Thus, these tax incentives allow employers to claim a refund on a portion of the paid tax and contributions on salaries, for salaries paid up until 31 December 2025.

This tax measure aims to encourage employment, especially in sectors where there is a need for additional labor. Employers planning to expand their teams should utilize this tax incentive, ensuring compliance with all prescribed conditions to qualify for the refund of the specified tax amount.

It is important to note that the tax incentives providing a refund of a portion of the paid tax on salaries for newly employed persons cannot be combined with other types of incentives for the same persons, except those that allow a refund of a portion of the paid contributions on salaries for those persons, as provided by the Law on Contributions for Mandatory Social Insurance. Therefore, note that these incentives have also been extended until 31 December 2025.

UPDATE IN 2026: This incentive has been extended once again, so it is in force until 31 December 2026.

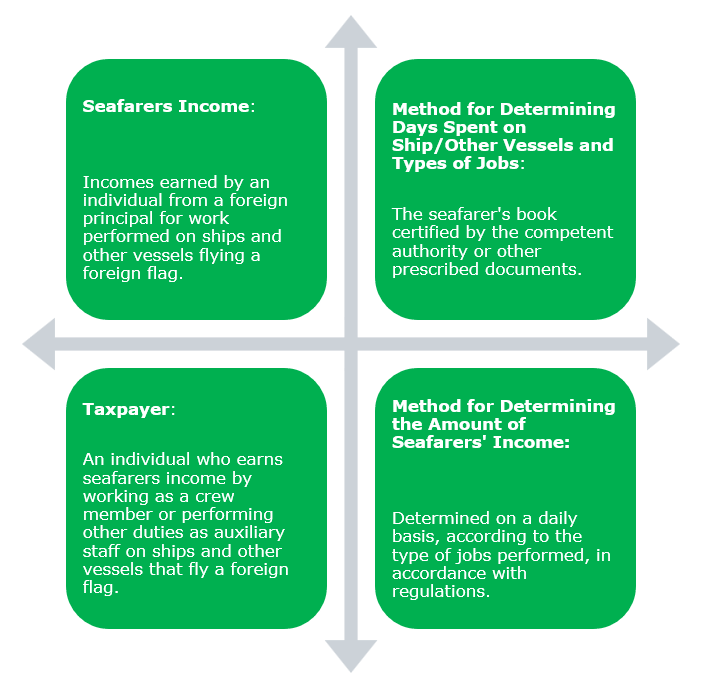

3) Tax Treatment of Seafarers’ Income

From 2025, provisions that explicitly regulate the taxation of seafarers’ income have been introduced into the legislative framework of Serbia. If you are a seafarer or plan to engage in this profession, this is information that could have a significant impact on your finances.

Here are the key details you need to know to comply with the new regulations:

- Taxable income of a seafarer:

The sum of the daily incomes of a seafarer, according to the number of days spent on ships and other vessels in a given calendar year.

- Exemption from the obligation to pay tax on seafarers’ income:

Seafarers who work on ships and other vessels for more than 174 days in the calendar year;

- The tax rate on income:

10%;

- Annual personal income tax:

taxable incomes of seafarers on which tax is paid are subject to the provisions of the Law concerning the annual personal income tax; and

- Filing of tax returns:

Must be submitted by 31 March of the current year for incomes earned in the previous year, and for taxpayers who are on sea voyage from 1 January to 31 March of the current year, within 15 days from the day of the first disembarkation in that year.

These amendments recognize the specificities of the seafarer profession and provide clear guidelines for the tax treatment of seafarers. The previous legal uncertainty regarding the taxation of this income category has now been eliminated, which facilitates easier compliance with the Law and reduces the risk of tax irregularities.

Seafarers and their employers should pay special attention to the records of the number of days spent on vessels as well as the type of work performed, using seafarers’ books or other prescribed documents. It is also crucial to determine the amount of income on a daily basis in accordance with relevant acts. The precise amount of seafarers’ income is determined based on the bylaw, the issuance of which is expected by the Ministry of Construction, Transport, and Infrastructure.

4) Increase in the Non-Taxable Amount for Daily Allowances for Business Trips Abroad

From 1 January 2025, the non-taxable amount for daily allowances for business trips abroad has been increased from EUR 50 to EUR 90. This increase reflects the rise in living and business costs abroad, allowing employees more adequate compensation for official travel.

This change enables employers to pay higher daily allowances to employees without additional tax burdens. However, employers are not obligated to increase the daily allowance amount to 90 EUR; this is the maximum amount that can be paid without being taxed. If lower daily allowance amounts are specified in the employer’s internal acts, such as the Employment Rulebook, employers may, but are not required to, align them with the new non-taxable maximum.

5) Changes in Claiming Tax Credit for Investments in AIFs or Purchasing Units of AIFs

Significant changes have been introduced concerning the entitlement to tax credits for investments/purchases in Alternative Investment Funds (hereinafter referred to as “AIF“). According to the new provisions, for a taxpayer to maintain the right to the tax credit earned, it is necessary to retain shares or investment units of the AIF during the calendar year in which the investment was made and for at least three calendar years following the investment year. Otherwise, if there is an alienation before the end of this period, the taxpayer loses the right to the previously earned tax credit based on that investment.

In the event of losing the right to a tax credit, the taxpayer is obliged to notify the competent tax authority within 30 days from the day of the loss of rights and pay the obligation in the name of the previously approved tax credit, along with the corresponding interest calculated from the due date of the annual personal income tax for the year in which the right to the tax credit was lost.

These amendments aim to prevent abuses of tax regulations and encourage long-term investments. Investors should carefully plan their investments, keeping in mind the obligation to retain investments in AIFs for at least three years after the year of investment to maintain the right to the tax credit. It is also important to adhere to the prescribed deadlines for notifying tax authorities in case of changes in investment status to avoid additional penalties.

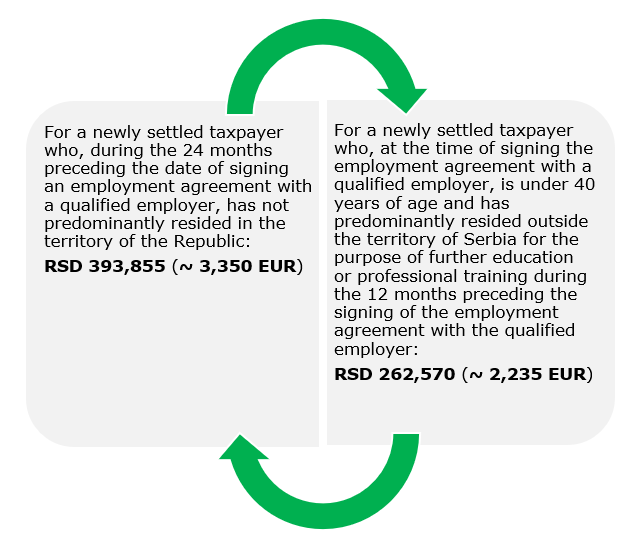

6) Changes in the Minimum Dinar Amounts of Monthly Salaries for Foreign / Returnee Employees for the Use of Tax Incentives (Article 15v, Paragraphs 5 and 6 of the Law)

In accordance with the latest amendments to the Law, which took effect on 1 January 2025, new minimum dinar amounts for the monthly salaries of foreign / returnee employees necessary to qualify for tax incentives on taxes and contributions for newly settled individuals have been established. Consequently, to utilize the tax incentive for employed foreigners/returnees who meet the prescribed conditions to be considered newly settled taxpayers, the minimum gross I salary now stands at:

Such adjustments are made annually; thus, the gross I salaries of newly employed individuals must follow the change in the minimum amount to continue meeting the conditions for using the incentives. Therefore, to continue utilizing the tax incentive for employed foreigners/returnees who qualify as newly settled individuals, it will be necessary to amend employment agreements with such employees if you wish to use these incentives in 2025.

UPDATE IN 2026: From the moment this text was first published, the amounts of minimum salaries have been adjusted again, and for 2026 they amount to:

- RSD 439,692 (~ 3,730 EUR) for a newly settled taxpayer who, during the 24-month period preceding the date of conclusion of the employment contract with a qualified employer, did not predominantly reside in the territory of the Republic, and

- RSD 293,128 (~ 2,485 EUR) for a newly settled taxpayer under 40 years of age who, during the 12 months prior to concluding the employment contract with a qualified employer, predominantly resided outside Serbia for the purpose of further education or professional training.

7) Aligned Non-Taxable Dinar Amounts of Personal Income Tax with the Annual Consumer Price Index in 2024

In line with amendments to the Law, the new dinar non-taxable amounts have been adjusted according to the annual consumer price index in 2024, with the application of these adjusted amounts beginning on 1 February 2025.

These amounts are regularly adjusted periodically, and some of them include the following:

- Non-taxable amount of tax on salaries based on the per diem for domestic business travel – up to RSD 3,380 (~ 30 EUR) per full per diem, i.e. the corresponding amount for half a per diem;

- Non-taxable amount of tax on salaries based on transportation allowances for business travel, i.e. for the use of a personal car for business travel or other business purposes – up to 30% of the price per basic unit of fuel multiplied by the number of fuel units consumed, but no more than RSD 9,855 (~ 85 EUR) per month;

- Standardized dinar costs recognized to freelancers – from RSD 107,738 (~ 920 EUR), i.e. from RSD 64,979 (~ 555 EUR), as applicable.

UPDATE IN 2026: From the moment this text was first published, the amounts of minimum salaries have been adjusted again, and for 2026 they amount to:

- Non-taxable amount of tax on salaries based on the per diem for domestic business travel – up to RSD 3,471 (~ 30 EUR)

- Non-taxable amount of tax on salaries based on transportation allowances for business travel, i.e., for the use of a personal car for business travel or other business purposes – up to RSD 10.121 (~ 86 EUR),

- Standardized dinar costs recognized to freelancers – from RSD 110,121 (~ 935 EUR), i.e., from RSD 66,733 (~ 560 EUR).

For a complete overview of all the adjusted non-taxable amounts, please refer to the official text of the Law.

To sum up, below you can see a brief overview of the key amendments to the Law on Personal Income Tax of the Republic of Serbia in 2025:

Interest Rates in Line with Arm’s Length – 2025 Regulation

In addition to amendments to the Personal Income Tax Law, significant changes have also occurred concerning transactions between related entities.

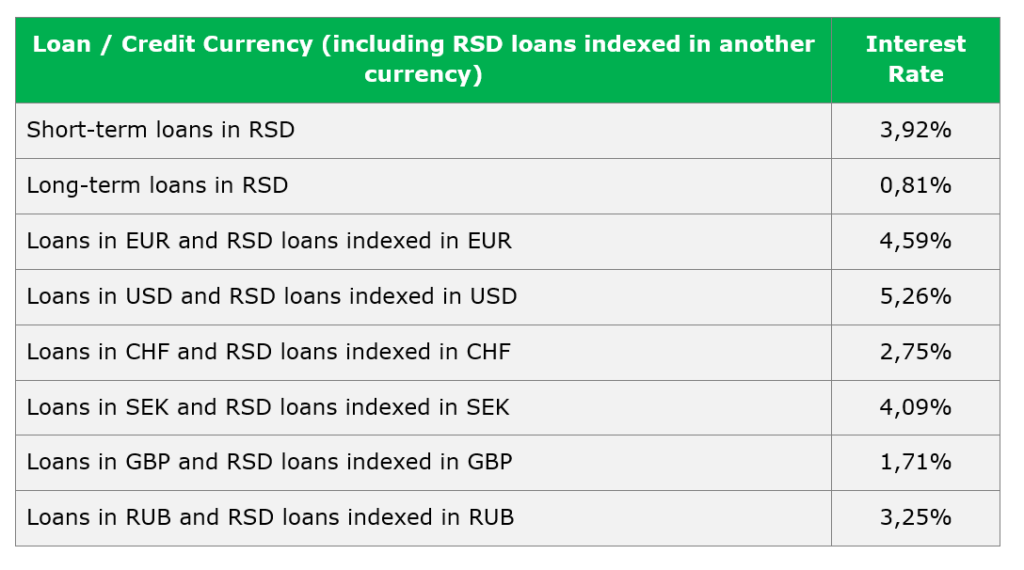

On 27 February 2025, the Ministry of Finance of the Republic of Serbia issued the Regulation on Interest Rates Deemed to Be in Line with the “Arm’s Length” Principle for 2025 (hereinafter: “Regulation”). This Regulation is crucial if you have or plan to enter into loan or credit agreements with related parties, as it precisely defines the interest rates considered market-compliant for such transactions.

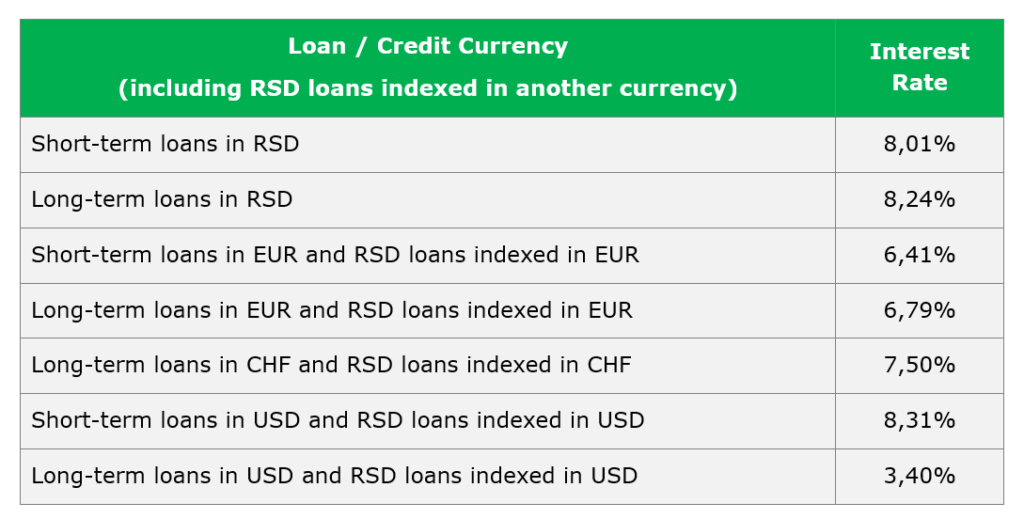

The Regulation stipulates different interest rates for banks and financial leasing providers, as well as for other companies, depending on the currency, indexing, and maturity of the specific loan or credit. The interest rates applied for the year 2025 are as follows:

For banks and financial leasing providers:

For other companies:

Since the Regulation is adopted annually, business entities should pay special attention each year to the changes introduced by the Ministry of Finance of the Republic of Serbia regarding the interest rates applicable for the following year. Continuous monitoring of these changes enables timely adjustments to financial arrangements, ensuring full compliance with applicable regulations and mitigating potential risks.

Tax Changes as an Opportunity for Business Growth

Although the tax reforms of the Law are a regulatory challenge, they are also a unique opportunity to enhance your business operations. By proactively adapting to the new regulations, you can optimize operational costs, take advantage of available tax incentives and benefits, and improve your competitive position in the market.

Serbian tax policy is increasingly oriented toward supporting innovative companies, as well as those that employ young professionals, foreigners, returnees, and highly specialized experts. These changes not only demonstrate the state’s commitment to fostering the development of innovative and technology-driven industries but also highlight a strategic goal of attracting global talent and further stimulating investment. A particular focus has been placed on sectors aligned with broader economic trends, such as alternative investment funds, thereby creating additional growth opportunities for companies aiming to address dynamic global challenges.

The key to success lies in a proactive approach: thorough education about all amendments, consulting experts in relevant fields, and adjusting business strategies to fully capitalize on the opportunities brought by these tax reforms.